Corporations own long term assets including tangible assets like buildings, intangible like copyrights, and natural resources like ore deposits. As it comes to value these assets there should be a way to devalue. To do that there are three concepts to know. Depreciation, amortisation and depletion.

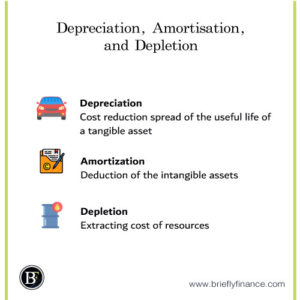

Depreciation is the cost reduction spread of the useful life of a tangible asset, amortisation is the deduction of the intangible assets and depletion is extracting cost of resources.

Quick Recap

In accounting not all figures are actual, there are numbers that are recorded in advanced or vis a versa in order to make a clear representation of the business performance and value in a certain time period which is called accrual accounting.

That is why assets in a company own numerically decrease in value based on the company judgement and based on the accounting accrual basis.

This is just heads up to let you know about why we reduce the values the way we do and why there are different methods to do depreciation.

Difference between depreciation amortisation and depletion

Attribution: The icons has been designed using resources from Flaticon.com

Depreciation

There are numerous methods to calculate depreciation. It is up to each company to choose the method that best suits its interests and the type of asset they own.

The reduction in value varies from one asset to the other. Thus you will have a separate depreciation rate for each fixed asset (tangible asset).

Here are the four most common methods for fixed-assets depreciation:

Straight-line Depreciation

The method is based on figure reduction, gradually, until the initial purchase value diminishes to the level of what is called “salvage” value. This term represents the estimated final ledger value of a specific asset after the final depreciation stage. This estimation is the amount that the company intends to receive by selling this asset at the end of its life span.

For example, let us say the company bought several new cars, as soon as they leave the showroom and the company want to sell them technically they lose value so when recording the transaction there should be an indicator of that reduction which is called depreciation.

Additionally, throughout the years these cars will tend to lose value because of their expected life value.

Straight-line method steps

- You record the initial purchase price for a fixed asset.

- Also based on common average values and experience, you will determine the item’s life span.

- Establish an estimative salvage value. This is usually determined based on the data on the asset’s market, and your own experience with this type of asset. When your asset reaches this level of wear, you have to stop using it and dispose of it.

- Then comes the calculation for the “depreciable” cost. This results after subtracting the salvage value from the initial purchase price.

- Divide the depreciable cost by the number of years decided for the asset’s life span. The resulting amount represents the value of your yearly depreciation for that asset.

Quick Example:

Asset: Factory equipment

Initial Purchase Price: $1000

Life Span: 5 years

Salvage Value: $200

Depreciable Cost: ($1000 – $200 =) $800

Annual Depreciation Value: ($800/5 =) $160/year

Double-Declining Balance Depreciation

- Identify Asset’s life span. Usually, after reaching the end of this interval (measured in years), the asset is no longer of any use.

- Calculate the depreciation rate. To calculate this, divide 100% to the life span value. Then the number obtained shall be multiplied by 2, and you’ll get the depreciation rate.

- Record the initial purchase price.

- Multiply the depreciation rate with the annual value of the asset. It will change as the years go by. Each year you will subtract the previous annual depreciation value from the asset’s value.

- In the years that follow after the salvage value was reached, you will no longer calculate any annual depreciation.

Quick Example:

Asset: Factory equipment

Life Span: 5 years

Depreciation Rate: (100% / 5 =) 20%; (20% x 2 =) 40%

Initial Purchase Price: $1000

Salvage Value: $200

Annual Depreciation:

Year 1 ($1000 x 40% =) $400

Year 2 ($1000 – $400(Year 1) = $600; ($600 x 40% =) $240

Year 3 ($600 – $240(Year 2) = $360; ($360 x 40% =) $144

Year 4 ($360 – $144(Year 3) = $216; $216 is close to $200 (salvage value) thus $216 – $200 = $16

Year5 $0

Here is a link to a calculator to further experiment with the numbers.

Sum of Years Depreciation Method

- Create a depreciation schedule, in table format. There will be 6 columns and one row for each year of the life span.

- The columns are as follows: Beginning Book Initial Value/ Total Depreciable Cost/ depreciation Rate/ Depreciation Expense/ Accumulated Depreciated/ Ending Book Value.

- Determine the initial purchase price and the salvage value. The purchase price will occupy the Beginning value column in the first row.

- All rows in the Total Depreciable Cost column are occupied with the difference between the initial purchase price and the salvage value.

- The Depreciated Rate column contains the number of each depreciation year (from the last one to 1). The general depreciation rate represents the sum of all years, as in 1+2+3+4….+x. And each row will indicate the years’ progression, as in x/x, … 3/x, 2/x, 1/x)

- The Depreciated Expenses column is calculated by multiplying the total depreciable cost with each corresponding annual depreciation rate.

- The Ending Book Value is the amount resulting after subtracting each year’s depreciation from the initial purchase price. This amount is also the number occupying the Beginning Book Value for the following year. And so on for each year

- This being a somewhat complicated table, I advise you to double-check each column and row. Here are some indicators that will show you if you did your math well. If you add all numbers in the Depreciation Rate column, you must get 100. The Accumulated Depreciation column needs to have on the last row the exact amount of the purchase price.

Indefinite Useful Life Method

This usually applies to lands. Unlike the other fixed assets, land tends to keep its value, even to increase. Only rarely land’s value drops. So in this case, the annual depreciation amount is $0.

Amortisation

Amortisation is an accounting technique that schedules the paying off an intangible assets over a certain period.

Amortisation Methods

There are several methods to calculate amortisation at a company’s disposition. Your choice depends on the asset type.

The amortisation process starts only when the respective asset is put to use. Keep in mind that for amortisation it doesn’t matter when the asset has been purchased. When you calculate amortisation you must take care to keep the book value in balance. It should not be overstated, nor understated.

Revenue-Based Amortisation

This is a method used for intangible assets. The amortisation rate is in direct connection with the asset’s contribution to the company’s revenue. Thus it generates variable amortisation rates. Being difficult to quantify and express in accounting the exact participation of an intangible asset to the general revenue, IAS 38 recommends not using this method. The straight-line method is preferred instead.

Straight Line Amortisation

This leads to a cover of the asset from the purchase price up to 0 value, or the residual value. It involves the book value (the initial purchase price), the useful life span (calculated in years), and the residual value. The formula that determines the annual amortisation amount is the following:

Amortisation = (Book Value – Residual Value)/ Useful Life Span.

Indefinite Life Assets

The method applies to indefinite life assets (for example the broadcasting rights or goodwill). The amortisation cannot be applied as for finite assets. Thus, for the indefinite ones, there is an annual impairment test being implemented every year. When the asset proves to be impaired, you have to make a life span estimation. Then the indefinite life asset shall be amortised just like a finite intangible asset for the rest of its useful life span.

Depletion

Unlike the first two indicators, depreciation and amortisation, which are applicable for all industries and businesses, depletion works only for the energy and natural-resources field (gas, oil, coal).

Depletion relates to the costs of extracting these natural resources. You could consider it to be similar to depreciation in the case of fixed assets. The depreciation indicator cannot work with energy and other natural resources, since they don’t have a useful life span. Thus, the depletion expense refers to the moment when the respective resource is being sold or used.

Companies cannot get a clear view regarding the exact amount of resources underground. Thus, the research, initial purchase, extraction, and further development costs are the ones capitalised for the natural resources, along the entire period they are being used.

Depletion Methods

Due to the particularities of operating with natural resources, companies cannot use the same methods as for depreciation.

The first step is to determine an average price for the natural resource unit. Then you have to calculate the depletion expense per unit. The formula is to take the total costs involved and subtract the salvage value. The resulting number is then divided into the estimated amount of total resource units. Then the total depletion expense is obtained by multiplying the depletion per unit by the number of units sold or used over a certain period.

For better understanding, I present you with an example. Let’s say that an oil company bought an oil field for $1 million. Their estimate is to extract from this land, 500,000 gallons. The average price per gallon is $2. If during the first year the company extracts and sells 100.000 gallons, the depletion for the first year is $200,000. For the following years, the company will register in its ledgers depletion expenses according to the extracted gallons, until reaching the $1 million, corresponding to the initial field purchase price.

Final Thoughts

These concepts are merely just ways for a business to categorise the value reduction of their items for easier reading. And those multiple methods are known ways to assist them in using different methods based on the type of asset they own.

Understanding these concepts can help you understand analysing companies, whether you want to do comparison or you just want to include your judgement in the way they depreciate their assets where you want to use your own method.

Related Posts:

- Accrual vs Deferral Accounting – The Ultimate Guide

- The 3 Components of the Balance Sheet Explained

- Common Components of Income Statements Explained

Disclaimer: Above links are affiliate links and at no additional cost to you. I may earn a commission. Know that I only recommend products, tools, services and learning resources I’ve personally used and believe are genuinely helpful and relevant. It is not because of the small commissions I make if you decide to purchase them. Most of all, I would never advocate for buying something that you can’t afford or that you’re not yet ready to implement.